Coming Soon! New Jumbo Offering

Great news! A new jumbo offering is in the process of being rolled out next week for Fairway Wholesale Lending.

Stay tuned for more info!

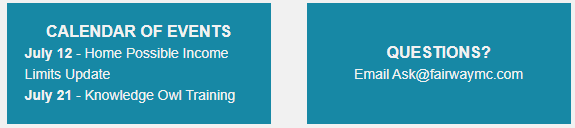

Register Today! Knowledge Owl Training Opportunities 7/21

As a reminder, Fairway Wholesale Lending is excited to be offering live Knowledge Owl Training opportunities scheduled for the 3rd Tuesday of the every month for our valued clients.

Knowledge Owl (KO) is the system in which Fairway's program guidelines are housed and are accessible by logging into DRIVER.

The training will provide the ins & outs of KO's functionalities and assist you with various tips for accessing guidelines in a quick and efficient manner, as well as allow the opportunity for you to ask any questions you may have.

Register below for this month's opportunity! You don't want to miss out!

July 21st @ 12 PM CST